Dissecting the Behemoth of Markets

Dissecting the Behemoth of Markets

Can this big fish, real-estate in fact predict recessions? Why is it that the housing sector takes up such a large portion of global market share?

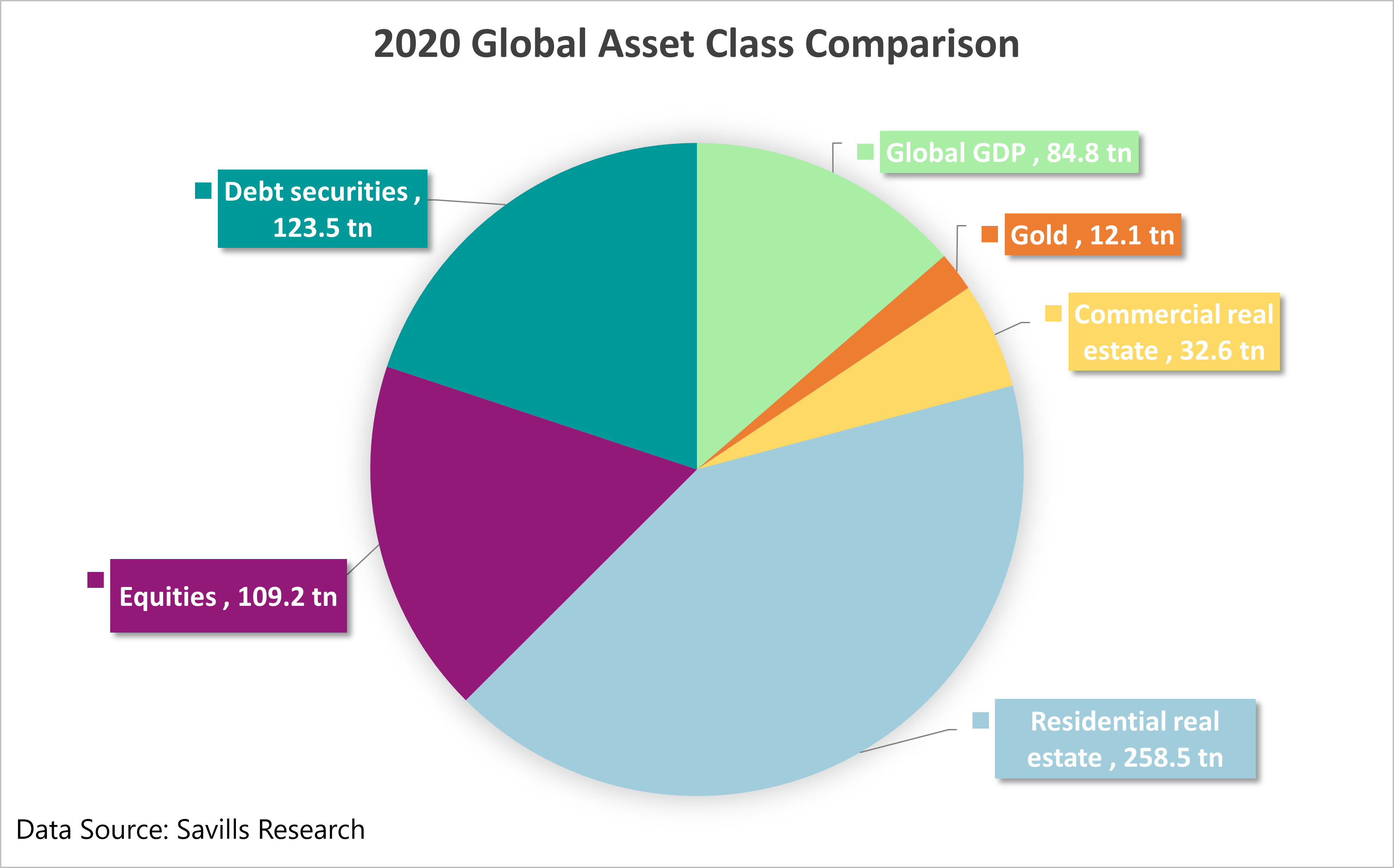

Real estate when compared to other market classes is by far the largest in terms of market cap, accounting for 46% (291 trillion dollars) of global capital. By contrast, equities account for 18% (109 tn) of the total market cap.

Why is it though that the housing industry takes up such a large portion of market share?

For one, real-estate investors and home buyers are highly mortgaged (levered), which expands the base purchasing power of these individuals and highly contributes to the aggregate market cap distributions shown above. For example, in Canada it’s not uncommon to see loan-to-value ratios of 80% or more, meaning the market has been largely fueled by credit, not cash.

Why is this important?

The housing sector is the most significant impactor in the productive force that drives the economic machine. In other words, the sustainability of real economic growth. Not only does it make up a large portion of household wealth, it also contributes vastly to the manufacturing, labor force, as well as other knock-on effects when a house is purchased (furnishing, appliances etc.)

Real-estate is pervasive, hence why this research will focus on the importance of housing and its role as a leading economic indicator.

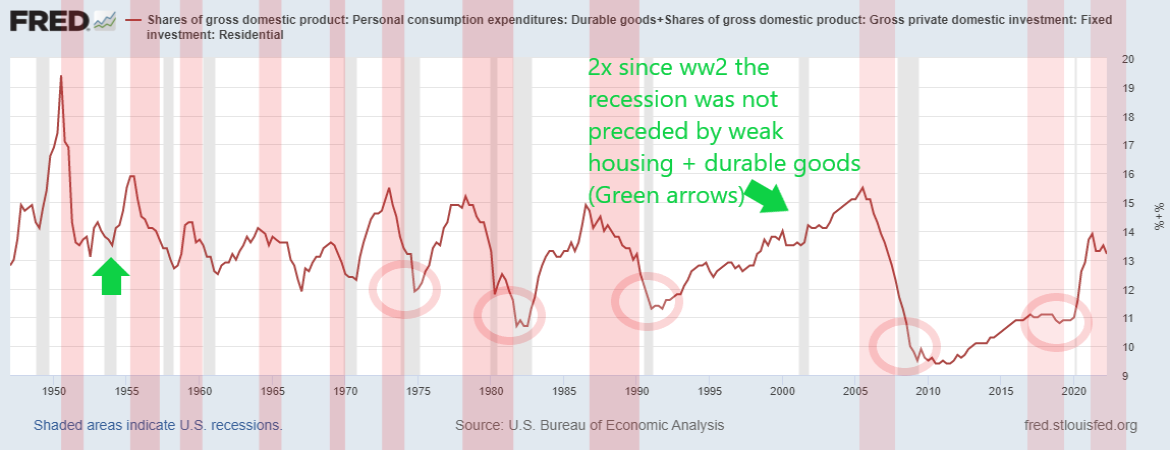

Since 1961, there was only one other time that a recession was not preceded by a major decline in the housing sector. In the graph below (figure 2.0) we take a look at the housing sector as percentage of nominal gross domestic product. In Canada and the U.S, we can see that when there was significant downturn in the housing sector (red arrow), a recessionary period followed (highlighted in grey).

The graph is tailored for the recessionary periods of the U.S so put your focus to the white line.

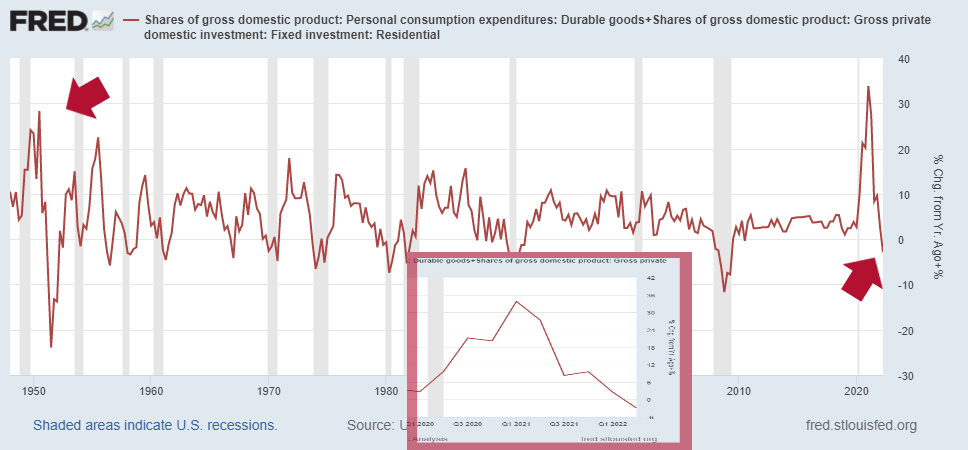

According to the analysis EPB research had done (HERE), both residential investment and durable goods had been the most effective in predicting future recessionary periods, hence why I followed up with a graph aggregating the two indicators together (figure 3.0).

Total residential investment is comprised of three items: new construction, renovation and ownership transfer costs. Durable goods, another leading economic indicator provides insight into the manufacturing sector - a major component in the overview of economic health.

The graph below indicates a trend reversal, but is it enough to say we are headed towards a recession?

Looking at this in relative terms (% change from one year ago), we experienced one of the quickest rises followed up by the quickest drops in history- witnessed only once before in 1953 (figure 4.0). This rate of change in both directions provides clues into how quickly the turnaround occured in the manufacturing sector.

The decline is likely due to the quick and aggressive rate hikes administered by the FED to tame inflation, indicating a sentiment turnaround by investors, business owners etc., who are now pricing in the rate hikes.

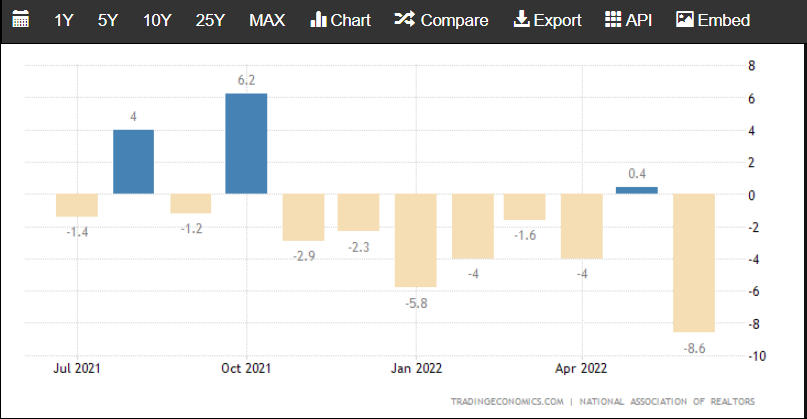

We can, in fact, quantify the sentiment of what these cohorts are experiencing (figure 5.0). This can be done by looking at the pending home sales index, which is a leading indicator of housing contract activity for: existing-single family homes, condos and co-ops. A method to assess the transaction volume of homes unsold two months after being listed.

When looking at the month over month data report, we can clearly see a significant reduction in home buyers volume, a trend that will likely continue as mortgage rates keep climb higher.

According to NAR, “buying a home in June was about 80% more expensive than in June 2019. Nearly a quarter of buyers who purchased a home three years ago would be unable to do so now. "Home sales will be down by 13% in 2022 but should start to rise by early 2023", Yun added. source: National Association of Realtors

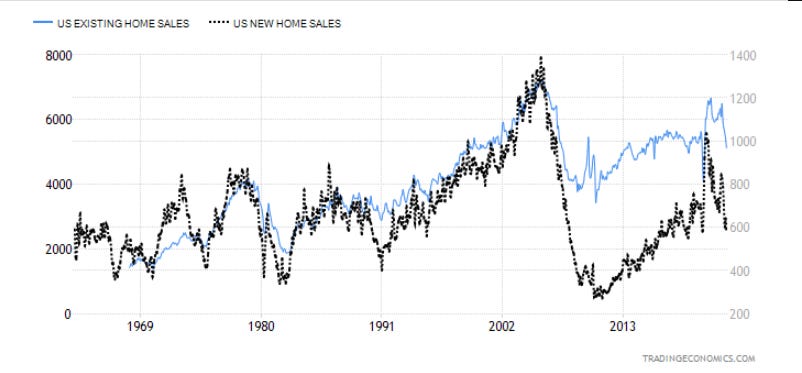

Synonymous with previous findings, housing activity based on the volume of homes sold (existing and new home sales) are also beginning to decline (figure 6.0). In his research, Leamer (2007) determined that it is “the volume of sales that adjusts not the price.” In other words, a reduction in housing volume is more indictivate than price itself, and that’s because of what follows after: weaker labor, finance and real-estate brokerages.

Given the sudden dip in housing, we can forecast many other sectors of the economy will feel similar repercussions.

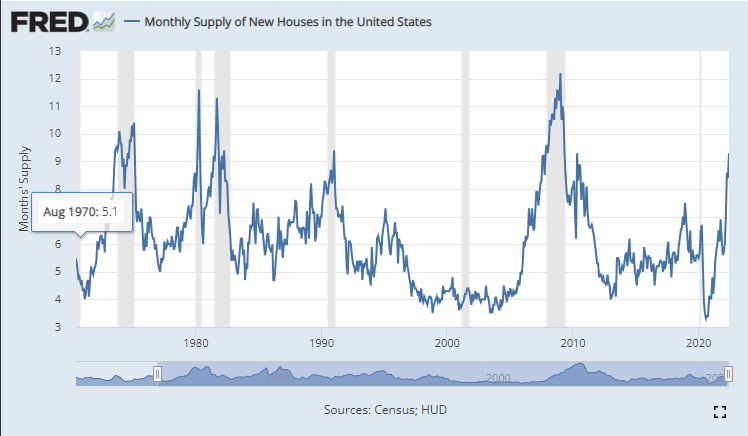

New home sales accounts for 10% of the US housing market, and the subsequent changes in the macro backdrop have caused a 8.1% decline month-over-month in home sales. The housing market is currently cooling after a decade long bull market. Now, with the cost of material and mortgage rates rising we have made homes unaffordable and businesses difficult to manage. Hence why we see this uptick in the monthly supply of new homes (figure 7.0).

The scale at which the housing market grew in 2021 was surprisingly strong - demand met supply and the housing market and productive force excelled. You would think that with all this historic data in mind, current trends seem almost parallel to the subprime bubble of 2008.

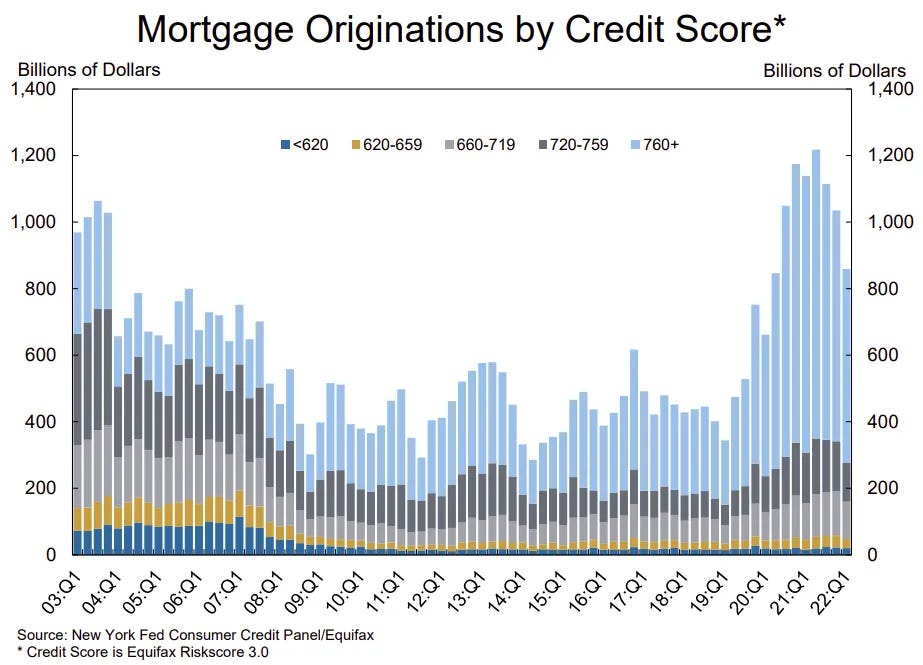

However, with solid lending, nominal prices of homes should stay stickier to the downside. In the visual below (figure 8.0), we can see a definitive change in the origination of mortgages when segregating participants by their credit scores. The credit scores can show us that this time, the amount of subprime borrowers has in fact changed (the data includes both purchase and refinance). There is significantly less subprime borrowers than there was before the 2008 great financial crisis.

The median credit score of newly originated mortgages declined again, to 776, down from a series high in 2021Q1 of 788. Yet, credit scores on newly originated mortgages remain very high and reflect continuing high lending standards.” (McBride, 2022).

You can find his article (HERE)

Does that imply we are out of the woods and prices are likely to become stable soon?

What can we expect moving forward ?

The data still forecasts further downside to the housing market, albeit a potentially less aggressive recessionary period than experienced in ‘08. Given that the volume-based components in the housing sector are currently deteriorating, price will likely follow until visible turnaround in the growth component of the economy. The tail can be told both domestically and globally. Unlike any historical parallels, we have never experienced these environmental circumstances - well the 40’s do come close.

Inflation is still rampant with no definitive signs of a reversal. Therefore, the FED is likely to keep raising rates to cool the dragon.

The NFP coincident indicator created by EPM macro, which aggregates: payrolls (employment), real earnings (income) and manufacturing hours (production), all demonstrating a clear sign of a growth depreciation.

Many strong economic countries that drive global trade and real growth are showing major vulnerability to credit constraints. Therefore, a continuous contraction in liquidity, ultimately leading to systemic defaults - especially at the level in which these countries are indebted. You can read more about this in my article (HERE).

Real estate has dire impacts on the state of the economy because it makes up such a large portion of individual and business wealth across economic sectors. For consumers to feel more confident, we need all the red alarms above to start a trend reversal. Otherwise, we can expect further downside and even lead into a prolonged recessionary period.

If you feel this has helped in way, share with other your fellow humans!

Best Regards,

NeuroInvest Analytics

Twitter handle: Neuro__Invest

A short disclaimer - I am a student of economics. I am not qualified to give financial advice. I am here because my fascination and obsession has led me to very credible researchers which I have found to be objective, open-minded and critical of their work.

References

Edward E. Leamer - Housing is the business cycle https://www.nber.org/system/files/working_papers/w13428/w13428.pdf

https://www.epbmacroresearch.com/