Bond Market Whispers

Bond Market Whispers

When the bond market moves, it cause seismic repercussions in the rest of the market.

After a long-awaited uptrend on speculative assets, does it seem like the market is turning around?

Well not quite, according to the data. In this article I will discuss what spurred this momentum to the upside and what the long-term data implies.

The FED decided to take a less aggressive stance yesterday (July 27), raising the FED’s fund rate only 75bpm. In response to this, a rally subdued.

We can get insight on these short-term moves by looking at how the bond behaves in response to these rate hikes. The credit system is highly dependent on the battle to suppress inflation expectations to the FED’s targeted 2%. Therefore, subsequent bond market moves can provide expectations of how the bonds perceive the future of inflation and nominal growth.

Why does the bond market care, and why is this important?

It is pivotal for them to care because interest rates provide insight into how accessible credit is in the short-term. Now that rates are currently rising, the bond market responds by demanding higher returns to lend their instruments. This is because they price in the future of inflation and nominal growth. The bond market essentially gives us a sneak peak into future market outlooks - they are a a proxy for predicting these expectations of growth and inflation.

The real rate does this diligently (figure 1.0 below)

This type of rate is considered predictive when the true rate of inflation is unknown or expected - a proxy for investor purchasing power. Basically, if rates rise, the cost to borrow or refinance credit in the short-term increases. Hence, the access to credit becomes much more expensive for the private sector. A very tactical approach by the FED attempting to suppress inflation.

As you can see above, since March we had real yields in negative territory. This tells us that we had an environment where levels of inflation were positive and interest rates were near zero meaning that you couldn't earn a positive rate return.

If you don’t know, bonds and treasuries are considered the safest most liquid form of investment. Therefore, if you want a safe haven for cash, you would be paying a premium to own bonds.

Why does this matter?

Well, investors at that point were less likely to invest in negative yielding bonds so they increased their risk exposure to equities and speculative assets, similarly to the price action in the last few days.

After yesterday’s meeting for example, the 75 bps point rate hike created new inflationary and growth expectations - specifically in 5y real yields. There was a decrease in the 5y, implying risk apatite increased.

The question is, is this temporary?

How do we know this risk on period is sustainable and have we found ourselves a new bottom for equities and value?

It’s the inflation that is driving the FED’s mandate to be more aggressive. When inflation is at a rate that has exceeded the ability for the FED to maintain governance, future expectations of aggressive hikes is likely not over. This is considering the historical measures where inflationary prints exceeded current rates.

How did the FED act in response to these historic circumstances? They kept progressively high rates and/or voluntarily induced a recession. According to @TXMC, “virtually all periods [CPI] was greater than 5% resulted in”

Raising Rates

Recession

TXMC pointed out in his graph above, only “twice has the US survived >5% CPI without high rates or a recession”. We have only two options to suppress inflationary prints.

If there is uncertainty about real economic productivity, then rates need to rise to compensate for the increasing rise of inflation.

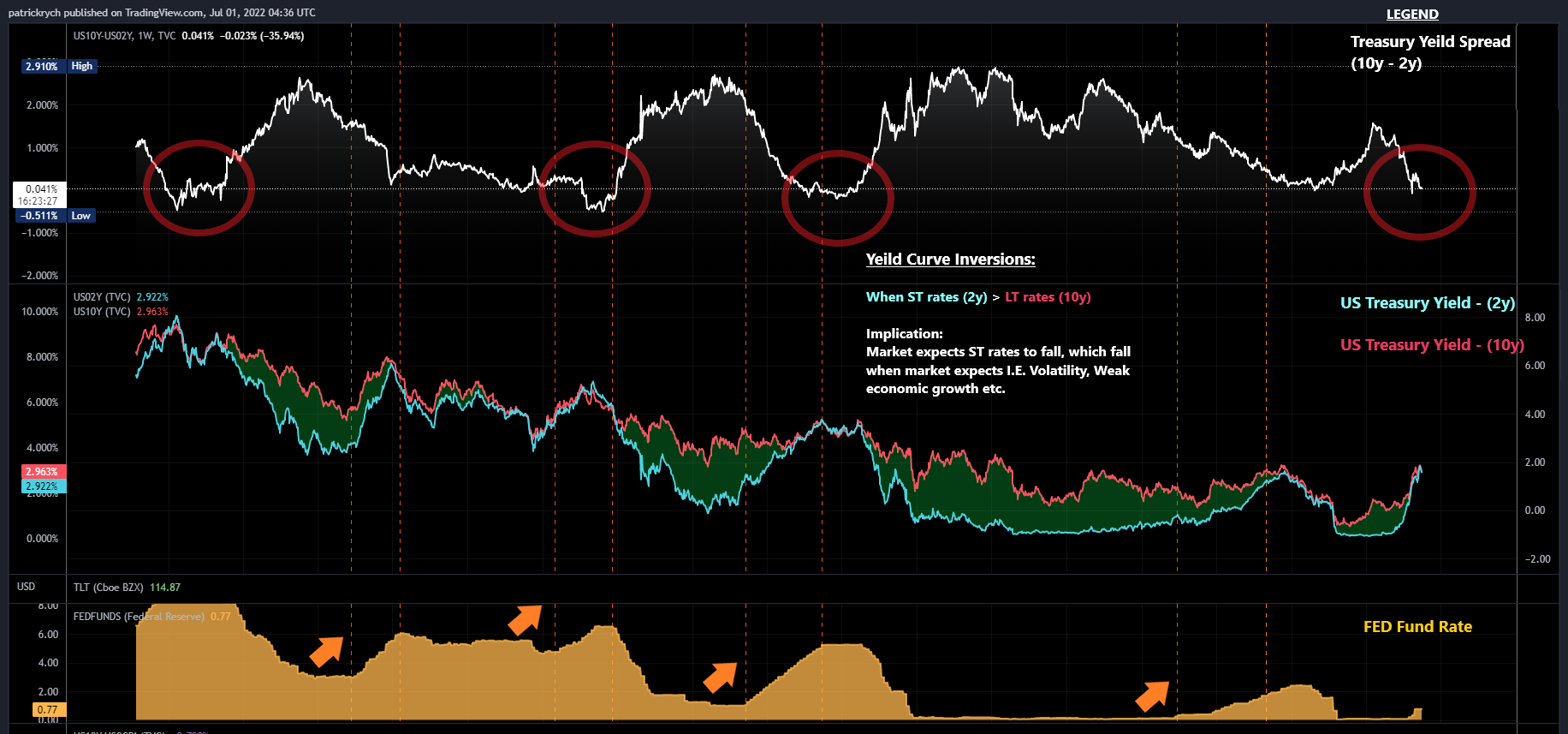

The graph above (figure 5.0), demonstrates the behavior of the FED funds rate. As the rate (orange) increases, the subsequent short end (2y yield in blue) moves upward toward the long end (10y yield in red).

As you can see, I pinpointed with orange dotted lines the times that the FED was raising rates. The FED lacks control over the long end (10y treasury yield: red) hence, the incremental increases in the FED funds rate brings up the short end (2y treasury yield: blue) towards the 10y. This creates what we know as yield curve inversion. This is the FED’s attempt to suppress demand and control inflationary prints.

As mentioned earlier, the cost to finance debt increases as rates rise. This creates stress in the financial market, structurally bringing down the productive forces driving real economic growth. So if you want my opinion, we have a ways to go before cyclical growth is affected in a positive manner and we witness sustained market rallies.

According to the data, the credit market still carries risk which implies a systemic decline in growth. What we can expect?

The private sector will need to pay a higher premium for the cost of credit and therefore further constrained liquidity and growth.

Value and growth stocks which are highly liquid are likely to move down towards their real valuations, if not further.

Aggressive and sustained rate hikes until inflation is coming down

A recession is imminent and growing day by day

Risk on periods are likely short and sweet

Wish you luck out there,

Mr. NeuroInvest

Stay tuned for more updates!

For more frequent updates I am active on twitter you can get quicker and more frequent updates.

Twitter handle:

NeuroInvest Research

@Neuro__Invest

References:

https://www.investopedia.com

Twitter: @TXMCtrades

You're articles are continuously making me think about these topics in whole new light. Keep up the great work!