Putting a Price Tag on Property: Are Canadian Homes Overvalued?

Putting a Price Tag on Property: Are Canadian Homes Overvalued?

A comprehensive look at the Canadian real-estate market. Looking at the valuations of homes, the true costs of owning a home and a quantitative outlook on future market trends.

Hello and welcome back to NeuroInvest Research!

For a prolonged period, real-estate created substantial improvements to the economy. All participants were benefiting from a seemingly endless equity boost. Have you ever wondered if the market’s energy could eventually slow down? Have these inflated home valuations been over extended?

This article will provide some much needed clarity into the various topics, which are mentioned in the abstract below!

Abstract:

Home valuations: The law of conservation of ‘economics’

Analyzing the Future Growth Trends

The True Cost of Owning a Home

Macroscope: Probabilistic Trends of Home Prices

What are the Chances of a Housing Crash?

The Law of Conservation of ‘Economics’

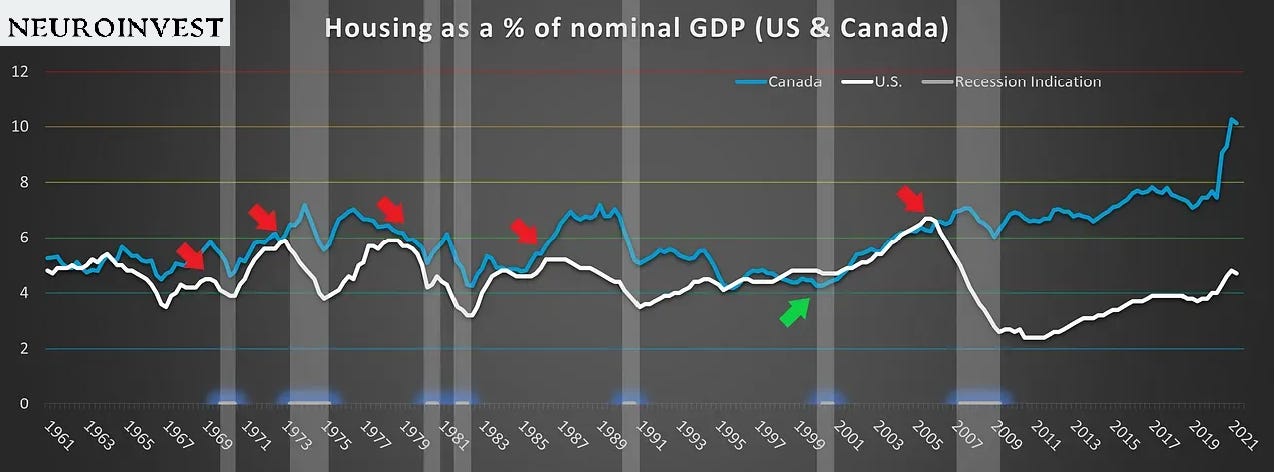

The Canadian housing market had accelerated rapidly throughout the 2000’s and was responsible to a large degree for the growth expansion in the economy (GDP). It was inevitable, since the production of a house has many knock-on effects. Including: labor (manufacturing, production), investment, business revenue (private and public), consumer spending and more.

The accelerating force of housing and its subsequent impact on growth can be reflected by the graph below: Canada’s housing market as a percentage of GDP.

Why is this important and what does this have to do with home valuations?

Well let’s break this down with an analogy which will hopefully shed some light on the probabilistic trends for real-estate valuations moving forward.

According to the law of conservation of energy: the greater an object’s mass (home market value), the more energy (cost of capital, supply vs demand) is required to move the object. Over the course of this housing expansion, there was a sufficient amount of energy that kept this object in perpetual motion. In fact, Canadian homes since 1997 exploded by a net total 196% as depicted below. The greater the pent up demand to engage in this business operation, the more kinetic energy was readily available to keep the object moving.

This analogy should help us unpack the various potential fuel sources that helped achieve the objects perpetual motion over the last 2 decades, as well as the requirements it will need to achieve a similar trajectory moving forward.

So until now, we had the energy to keep the ball moving, uphill rapidly.

Strong demographics

Labor strength

Cheap and ‘easier’ access to credit

Strong economic growth

Asset inflation (base money growth)

Money supply Growth (broad money growth)

Lower private and public debt levels

This economic expansion (GDP) created vast amounts of wealth, giving participants the ability to pay premium for real-estate. It was an endless feedback loop that ignited the fire of spending, saving and consumption.

The cycle continued, especially for the Canadian housing market, as it was only marginally set back by the great financial crisis.

However, the growth of home prices was continually augmented by the use of leverage. In other words, credit that fueled a large degree of economic output. This credit abuse was largely responsible for making housing unattainable for most.

Note: Credit is an elastic force that can help facilitate the growth of economic activity and to a certain degree, it definitely does. However, it also has dire effects when environmental changes suddenly occur and there is too much debt circulating in the economy.

Today, it may be quite a bit more difficult to sustain the object’s momentum.

Here’s why.

The energy impeding the potential of growth moving forward:

Weak demographics (working class populous, home buyer cohort)

Cost of credit (interest costs moving up on inflated valuations)

Federal Reserve and government deficits (i.e., increased taxes)

Supply restrictions with the geopolitical conflicts causing cyclical and potentially secular inflation

Law of large numbers

Disposable income relative to home prices at record highs

Investing today: A Mock Evaluation of a Real-Estate Investment

Before we touch up on these environmental factors, let’s run a mock analysis.

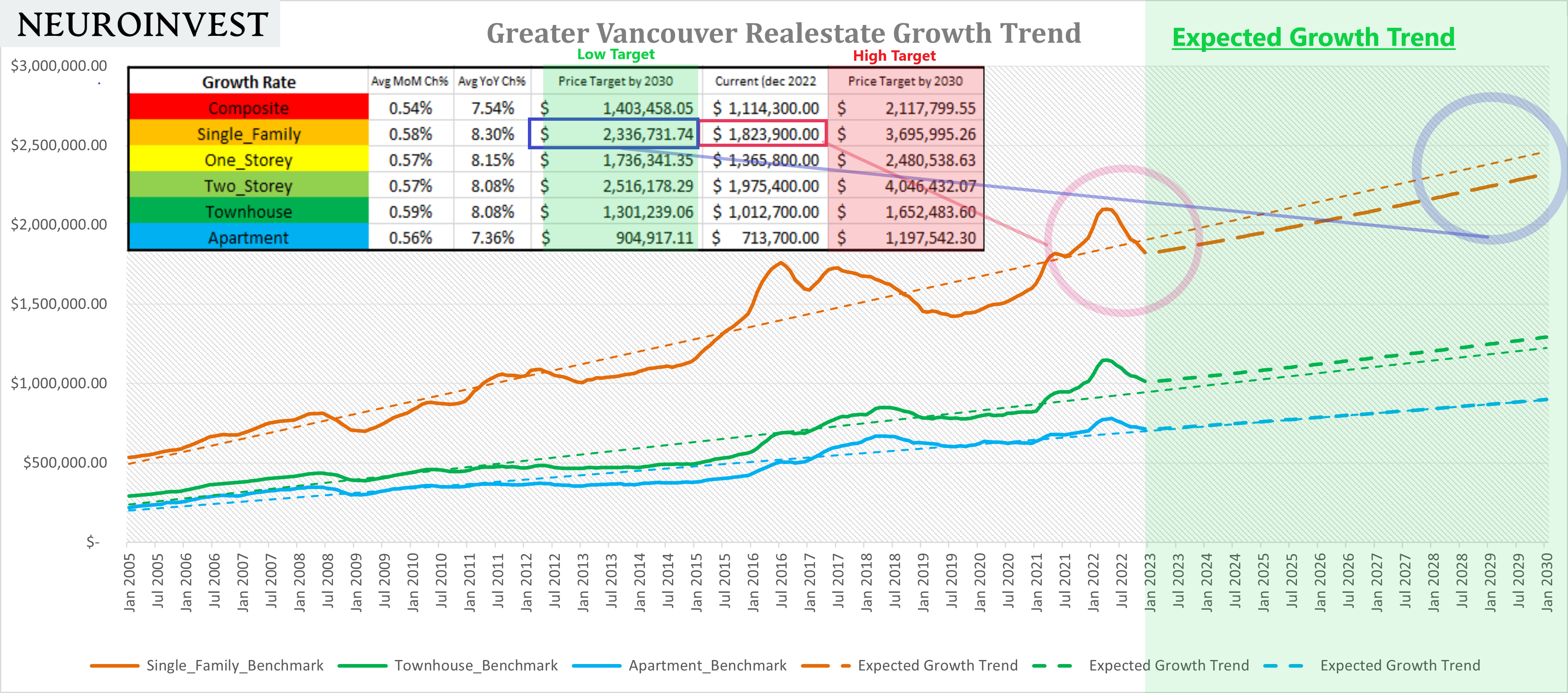

Let’s say you decided to purchase a home today at $1 million. Assuming we have a growth rate that remains unchanged (7.54% YoY - this # is based on the average growth rate throughout the 2000’s - 2021 period), the average price of a home in 2030 would reach $1.6m.

To note: 7.54% is based on the average growth rate of homes in Greater Vancouver. This is a composite metric - meaning, the average of all sectors of housing in aggregate (single family, townhome, apartment).

Also it’s important to know, in the analysis you’ll see a LOW and HIGH target for this expected path of homes. The graph below shows the value of homes today and their projected valuation, based on the yearly growth trends.

Let’s start off with an optimistic outlook. The home bought back in 2023 had achieved the HIGH target growth rate of 7.54% YoY. The home appreciated 28% by 2030 and gained you a net profit total of 600k.

That seems like a great investment, would you not say?

Well, that very much depends.

The True Cost of Owning a Home

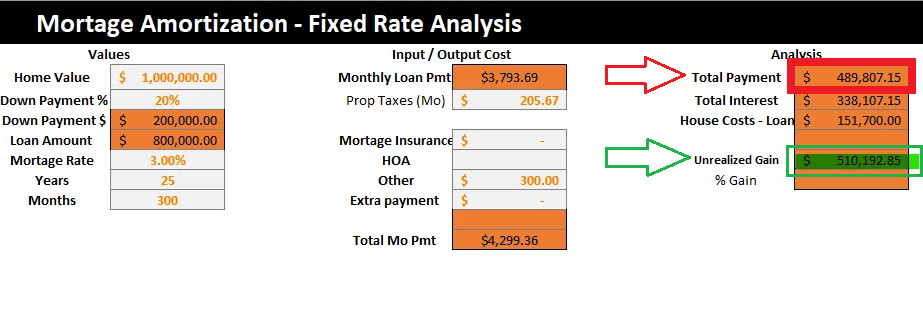

A house at $1 M, with a down payment of 20%, leaves you an 800k loan amortized for 25 years, assuming a mortgage rate average at 3%. Over the course of your contractual agreement, the total payments to hold the asset cost: $489,807.15 - the deadweight cost.

More importantly, what is our profit?

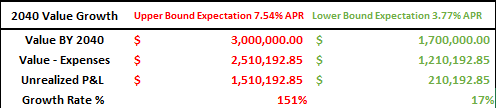

Well, by the time your contractual obligation ends, once again, assuming the growth trends remain unchanged (HIGH and LOW) - in 2040 the total net total profit on the home would achieve 1.5mill (HIGH) and 200k (LOW) - as shown below.

Despite the positive values, they both show tremendously different levels of net profitability.

Yet, we are still left with the fundamental question - are these valuations likely to remain on this expected growth trend, or is this analytical consideration too optimistic?

What if the conditions have changed?

Considering we are in a vastly different economic standard today, the exponential growth trend in housing may be unrealistic. Of course, I cannot state such a bold claim without evidence to prove my point - so here is the synopsis.

Macroscope: Probabilistic Route

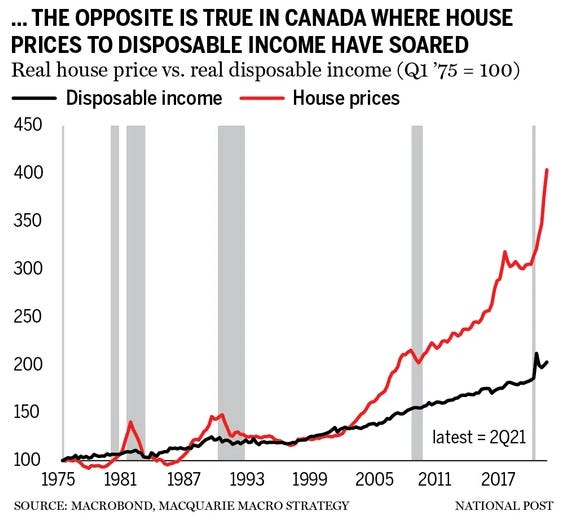

First and foremost, Canada is ranked second of 38 developed countries to achieve the highest home price valuations. This is a home affordability metric that is measured by looking at the ratio of house prices-to-disposable income. (Guiao, 22) Today, Canadian homes are priced 17x that of average income. In other words, these homes are far out of reach for most - the valuations have spread far beyond the ability to afford them.

The continuation of these valuations largely depends on the on the trajectory of economic environmental conditions (monetary policy).

Environmental conditions?

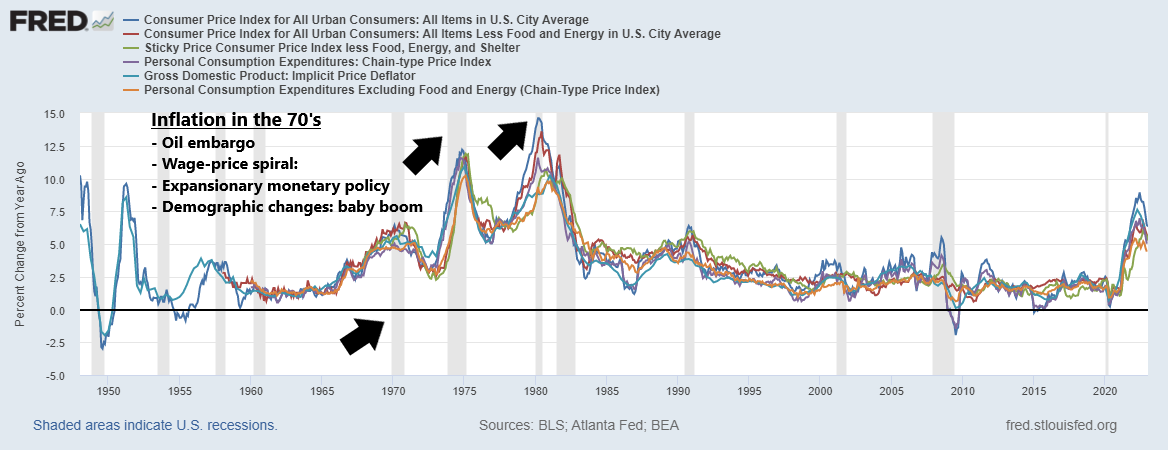

There is a large debate whether inflation will remain sticky to the upside, reminiscent of the inflationary period of 70’s. Yes, we are currently in a deflationary trend. However, the volatility of inflation remained high in the 70’s so what are the chances we get to see a deflationary trend today and more importantly what effect do these aforementioned environments have on homes values?

With the generational reliance on cheap imports and many geo-political conflicts, it is unlikely that inflation moves away swiftly. Since the FED changes rates in line with inflation, it is no question that you could be paying a premium to hold your investment over the course of the next couple decades.

Today, the federal fund fund rate is still moderately below the inflation level. Which is why we’re seeing rates still elevated today. They will likely remain higher for longer if inflation stays stubbornly high. Currently the BoC has the rate pegged at 4.5%.

All in all, if we’re likely to have inflation stay higher this decade, profit margins may look thinner for speculators.

Secondly, demographics are looking slim for the working class populous, which favors the deflationary argument, but also limits the fuel that could spur demand for home appreciation. With less economic input (labor participants, wage growth etc.,), we have less economic output (growth in GDP).

In addition, the levels of debt that has compounded in the private sector in the last few decades also limits the degree of sustainable economic activity moving forward. With large business operations being this dependent on debt, delinquencies are becoming increasingly more apparent.

A major developer with $1 billion worth 1of prime property in Vancouver and 16 projects on the go is filing for creditor protection. Coromandel Properties Ltd. has submitted a petition to the Supreme Court of B.C. for relief under the Companies' Creditors Arrangement Act. (Charach, feb 10, 2023).

This one example may not seem cataclysmic, but rates are still being digested by the economy. Moreover, with this much historic reliance and on debt to fuel assets, how will the environment look when the punch is taken away from the party?

Is this the breaking point of Canadian homes?

That really depends how well the private and public sector are positioned for the current economic downturn. Are balance sheets in the private and public sector equipped to handle rates for prolonged periods?

There has already been a drastic change in prices so far. As well as a picked up activity in credit default swaps. It’s difficult to say, but some of these super inflated real-estate markets, (BC, Ontario), are at risk for some contagious credit busts.

The future is unknown, but so far it doesn’t look pretty. Which is why BoC decided to take a pause and see how well the market is able to handle the elevated rates. Nobody wants a 2008 global financial crisis, the meltdown impacts everyone in the business.

Unfortunately, it is not entirely in their hands to control the level of these rates. At large, the FED has the power to influence other banks decisive actions - ultimately it is a game of currencies and trades.

Note: If you're curious about this you can read about the dollar milkshake theory by

We’re just in the thick of it, hoping that our monetary gods can find a silver lining in this wretched economic prognosis.

Conclusion

Despite all the potential reasons for real-estate to vere of-course from it’s normative pathway, we never know the actual route the market will take. There is a lot of money still floating around from the last decade of easy money (fiscal- and monetary-stimulus). Given all these circumstances and the use of our mock analysis, we can add the use of heuristics to assume a probabilistic range of estate valuations. Shedding some much needed light when making our quantitative decisions to own a home.

This by no means should deter you from buying a home. In fact, many market participants actually benefit from having these fixed payment obligations, regardless of the investment outcome. Maybe the growth rate won’t trend as it did, but that does not mean over the course of owning your home, it won’t appreciate in value. Moreover, you can always find novel methods to help offset these tight margins (finding a renter, tenant, increasing the cost basis on your home).

Thank you for reading, if you have any questions or comments, do not hesitate to ask. Also, if you are curious, I have made the document to determine the cost of your home freely available for you!

Check it out!

Signing off, NeuroInvest

ctvnews.ca/vancouver-developer-seeking-creditor-protection-facing-700-million-in-debt-

Once again a phenomenal article. Sucked me right in at the title. It’s going to be interesting to see where the market goes, especially in Vancouver!