Illuminating Lights of a Recession

There’s signs of major economic distress brewing underneath the monetary landscape.

Welcome back to NeuroInvest Research!

The U.S. economy seems to have avoided a full-blown financial crisis following the collapse of Silicon Valley Bank, but there are growing concerns about credit availability in various sectors.

The federal reserve's rapid pace of increasing rates to suppress economic activity is beginning to trickle in and become more tangible - as has been mentioned in previous articles.

Recent data suggest that lending has contracted significantly, small businesses and regional banks are showing signs of increased borrowing difficulties. Bankruptcies have risen among private companies in the construction, healthcare, and retail sectors. Financial analysts warn that more defaults may occur as lending standards tighten and the effects of the Fed's rate hikes continue to permeate throughout the economy.

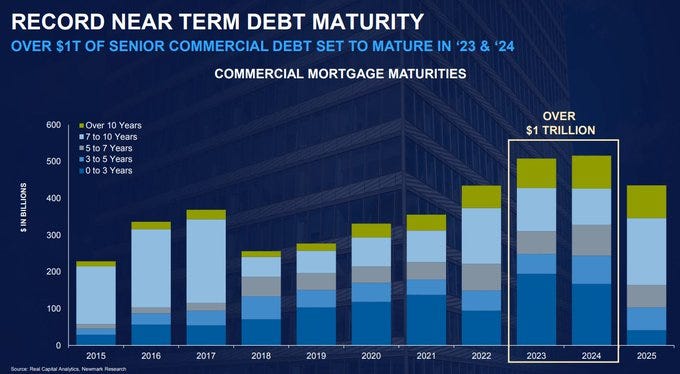

@RadicalAdem presented an example, specifying the distress in the commercial real-estate sector, he says: “there is over $1T of senior commercial real estate debt maturing over 2023-24.” 1

The problem is, the prolonged decade of low rates caused entities to finance their operations with instruments yielding rates close to 0. In the coming next couple of years, according to Adem Tumerkan, over $1T CRE loans will expire, and that debt will be looking for a new home.

To get an understanding of this, I will explain how these instruments are typically used in the monetary system, and their relevance in regards to the weight of risk that this imposes on the system.

Typically, institutions borrow money at short-term rates (ST) and lend at longer-term rates(LT), profiting from the difference. It’s an arbitrage opportunity until the long-end of these debt instruments start to incur major setbacks. That happens when interest rates rise; the price of a bond with a higher duration falls more than that of a bond with a lower duration.

Investor’s don’t lose their present value if they hold to maturity, only the opportunity cost, as they could have earned a higher yield for bonds that were priced today at a higher yield. However, those circumstances change when the investor decides to sell in the open market. In that situation, the present value of the bond’s future cash flow needs to be discounted by the effect of the current rate, which today, is significantly higher.

This is a period that has escaped historic analogs, explaining why the infamous 60/40 portfolio has failed to provide portfolio stability.

Self-Fulling Credit Bust

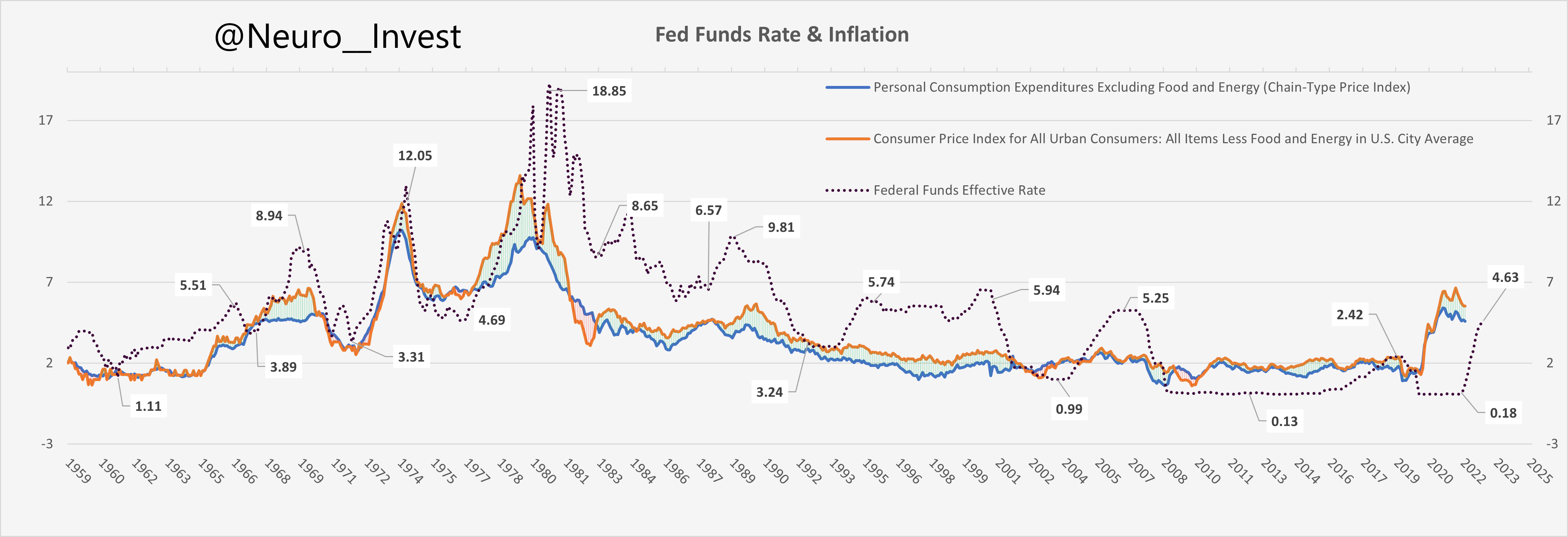

A clear illustration of the current economic distress can be seen by examining the yield curve, which compares short-term interest rates to long-term interest rates (refer to Figure 2.0). Typically, a healthy yield curve exhibits an upward slope, indicating that investors expect higher returns for taking on risk. However, when the yield curve flattens or inverts, with ST rates surpassing the LT rates, alarms begin to flash warning signals.

Furthermore, we’ve been negative for quite some time, and inverted yield curve take some time before they negatively impact financial institutions, particularly banks, which rely on those arbitrage strategies to stay profitable.

Similarly to the example used above, a large amount of CRE loans are on the brink of expiry and will need to be refinanced. However, with the expectations of risk, banks are less likely to lend and face the potential of loss on their books.

Moreover, CRE loans over the last decade have increased significantly - adding over $400 billion of debt which is expected to mature this year.2If these loans can’t find a new home, commercial property owners could be forced to liquidate their positions.

It’s this negative, self reinforcing feedback loop that could create major distortions on the credit system; specifically for smaller banks, which have increasingly forged new loans throughout the last decade.

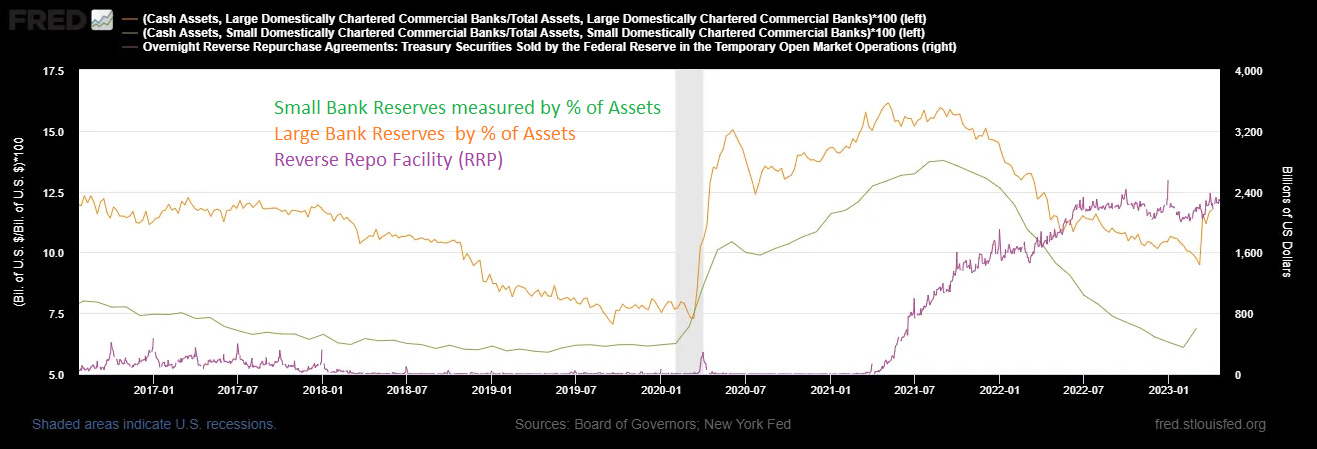

Small banks which are highly exposed to CRE loans are demonstrating that their cash requirements are unequipped to handle major outflows, or take on major risk.

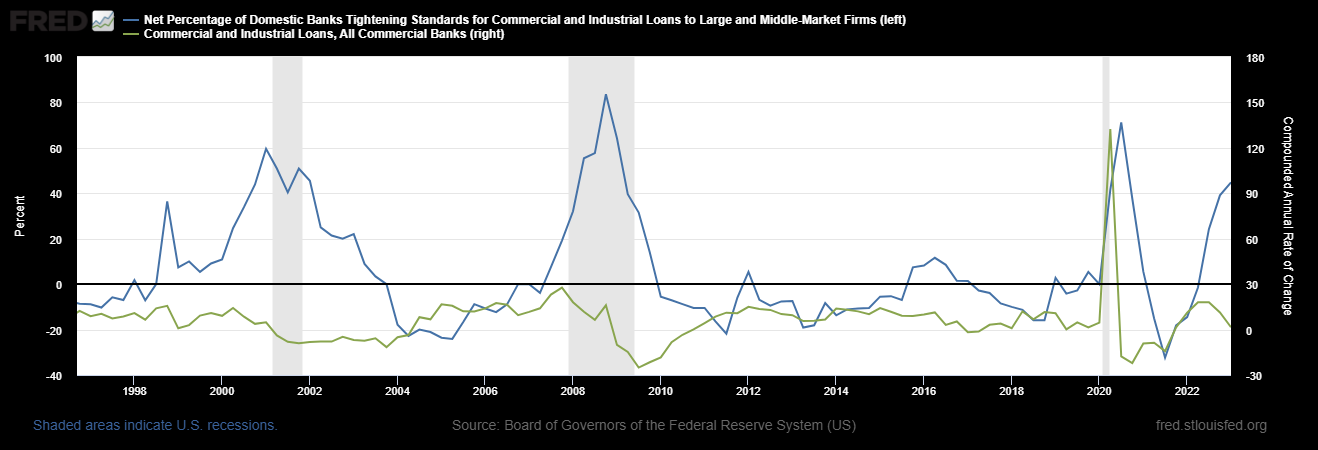

This is also shown when we see the signs of tighter credit conditions, shown below. More importantly, banks have now significantly increased their lending standards, and commercial loans and banks have followed suit.

Through all this transparent turmoil - the Reverse Repo Facility (RRP) which currently holds $2.72T has barely moved in response to these liquidity stressors.

What is the Reverse Repurchase Agreement (RRP): It is a tool used by central banks like the FED to control the floor of interest rates and manage excess cash in thefinancial system. By temporarily selling securities to banks and other eligible participants, the central bank effectively provides a safe, ST investment option. The RRP helps maintain desired interest rates and supports monetary policy objectives by offering a risk-free investment alternative, which ultimately contributes to the stabilization of financial markets.

Those who are eligible, park their excess cash with the central bank in exchange for treasury securities on an overnight basis, effectively earning a modest return on their funds- this is done with the RRP. But, without any conditions set on the RRP, why would these entities take their capital elsewhere?

Moreover, the $2.72T sitting in a black hole, and is not available to those entities who are desperate for collateral and protection - it’s causing a major disconnect in the monetary system.

Ironically, the FED uses these market operations (RRP) to manage short-term interest rates and excess cash in the financial system, and letting go of this lever could reignite the inflation dragon once again. That would lead us back to square one. Similar to the 70’s period, when Burns (1970-1978) served as the federal reserve chairman.

Absentmindedly, the Fed continues their quantitative tightening (QT) program to suppress inflation, committed to deflate CPI back to their target 2% range.

How far are they willing to go before the economy is broken? I believe we’re close, and i’ll keep you informed, there is much more to talk about then presented here.

Otherwise, I hope you found this to be interesting or helpful, please like and subscribe - it helps tremendously!

NeuroInvest Signing off…

https://www.bloomberg.com/news/articles/2023-03-22/bank-turmoil-ramps-up-pressure-for-900-billion-of-property-debt?sref=nD2OD0Ri#xj4y7vzkg - John Gittelsoh

https://www.lynalden.com/march-2023-newsletter/