Monetary Blueprints: The Treasury, the Federal Reserve, and the Banking System

Have you ever thought about how money is created, how it circulates throughout our economy and the subsequent impact of these intricacies?

Have you ever thought about how money is created, how it circulates throughout our economy and the subsequent impact of these intricacies? The processes that guide the creation of “money”, the flow of funds, the direction and health of the economy, all develop from the interconnected web of central banking. The FED, the Treasury and the banking system are integral to the structural health of our monetary driven world. But how is money actually created - who, when and why do they make these decisions, and of course how does this impact the broader market. This article, which is the first part of many article series on monetary mechanics, aims to dissect the mechanics underlying these musings, in hopes to help you further understand the modern day financial ecosystem.

Let's start with the government and some basic accounting principles. Much like any financial participant, the government is an operative business - be it an individual, multinational corporation, the government too has obligations to cover (debt). It may not come to you as a surprise (since it’s on every headline), that the U.S government is currently running at a large deficit, and that will continue as long as the revenue spending (federal outlays) precedes the amount of revenue (receipts) they bring in. This is unlikely to change, and in fact will only progress, by the CBO’s own projections.

Why is this important? Because when the government spends into the economy, they’re effectively creating money to support the financial systems needs. This becomes one of the many forms of money creation. Let’s dive a bit deeper into how these mechanics actually develop in the financial ecosystem.

“Federal government spending pays for everything from Social Security and Medicare to military equipment, highway maintenance, building construction, research, and education. This spending can be broken down into two primary categories: mandatory and discretionary. These purchases can also be classified by object class and budget functions.” 1

Synthetic Fiat

As mentioned, the spending thus far has exceeded the expected revenue being generated - because of this, the Treasury account balance quickly declines. This is why they issue more debt. From the perspective of the Treasury, instead of taking a loan like an individual might from a bank, they issue securities in the form of debt. It's akin to saying, “Lend us some money now, and we promise to pay you back with a little extra as a thank you.” This 'extra' is the interest.

Figure 1.0 - The FED controls the size of its balance sheet, and the Treasury Department controls the size of the Treasury General Account. When the Fed expands its balance sheet by creating reserves and buying bonds, it is injecting liquidity into financial markets. When it reduces its balance sheet, by being a net seller of bonds and destroyer of reserves, it is removing liquidity from financial markets. When the Treasury expands the TGA, by raising debt and bringing in taxes faster than it spends money, it is sucking liquidity out of the system into a void. When it reduces the TGA, it is spending more money into the economy than it is currently withdrawing, or in other words putting liquidity from that void back into the economy. So, the smaller the TGA, the smaller the void of dead capital. There are some months where the Treasury can be injecting liquidity while the Fed removes it, or vice versa.

A second question arises: Who buys the debt and does it in fact increase the money in the financial system ?

Those designated as primary dealers are significant buyers of government debt. Their substantial purchase of Treasury securities is not just a mundane operation but a crucial cog in the wheel of financial markets. These banks, such as JPMorgan Chase & Co., hold these securities either as investments or use them in financial operations. The incentives to hold government debt are two fold: risk premium and regulatory requirements

For one, financial players can and do have a choice to buy the debt, but their choice is highly dependent on their preference to take on the risk in the first place. In other words, an entity's willingness to purchase a financial instrument is a function of the risk-adjusted returns (comparing other yields, assets discount rate etc.,). This is commonly referred to as risk-premium. If the risk-premium is too low, what incentives do these entities have to purchase the debt? In short, the answer to that question is - they don’t, which is why capital will look for alternatives. This drives down demand and props up yields on these instruments to maintain investor interest.

Bill issuance is the quickest way to rebuild the TGA quickly or finance short term spending needs. When the Treasury needs to monetize their spending, they’ll issue debt, and that debt is purchased by exchanging the assets (treasuries) with the banking reserves held in the banking system. However, what's commonly misunderstood during these mechanisms is that throughout the process, the Treasury does not create money, it reshuffles it.

To continually spend into a deficit the government effectively creates an overdraft in its account at the FED. The recipient, being the financial sector, sees the increase in bank deposits. However, the problem is that the government is running such a large deficit, they essentially exchange their financial instruments with the pre-existing deposits which were initially deposited by the government. This literally further exacerbates the gap between federal outlays and receipts, as their strategy to pay off existing debt, is with more debt.

Deficit Spending = Private Surplus

Debt Issuance + Deficit Spending = Liquidity Reshuffling

One Ring to Rule Them All

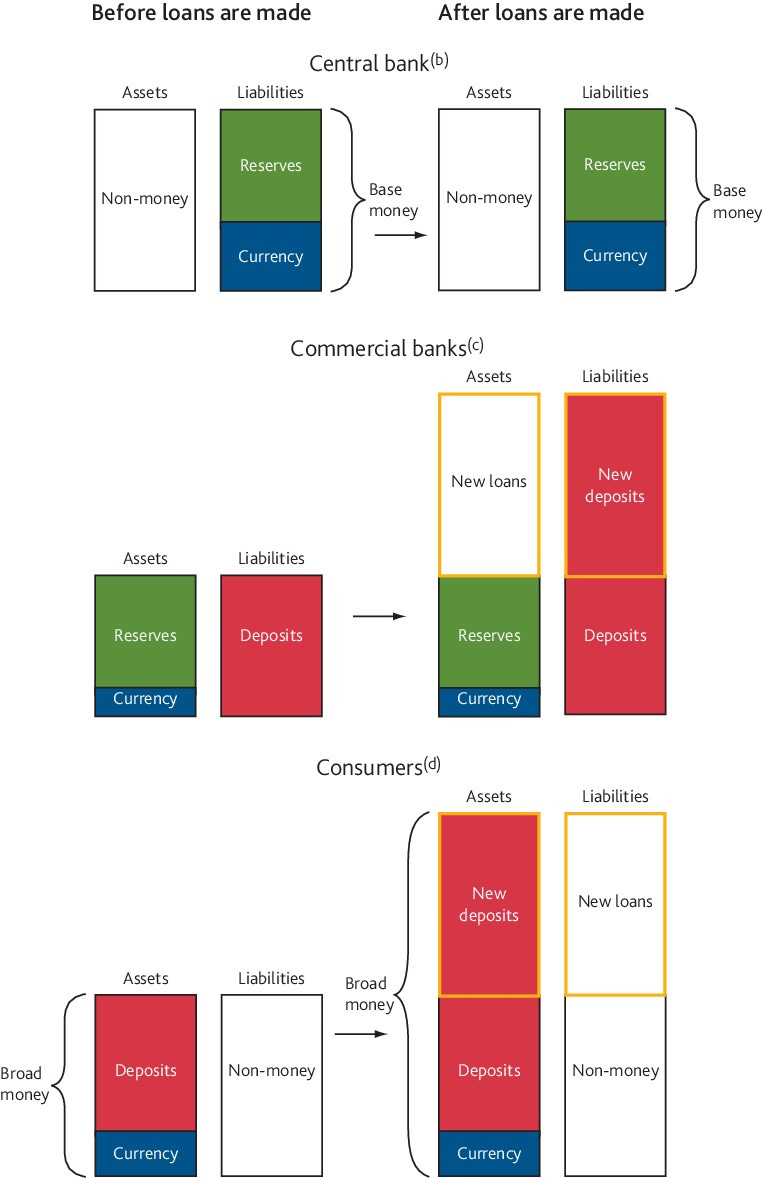

Central to all liquidity flows is the Federal Reserve (FED)- which has the ability to influence the amount of base money (or "high-powered money") in the system, which consists of currency in circulation and bank reserves. This base money serves as the foundation for the broader money supply, which includes various forms of money like checking deposits, savings accounts, and more. The FED can create (or destroy) bank reserves through its open market operations, and they are the most influential central force to liquidity flows in the financial system.

The FED has the ability to create these reserves “out of thin air”, but does so with purpose in mind. For instance, the FED needs to maintain a minimum holdings of bonds and notes which they passively acquire from the Treasury. Conversely, when the Fed sells securities to banks, it debits their reserve accounts. So you begin to see, the FED uses its open market operations (OMO) to justify their financial obligations, but also OMO is used to primarily manage short-term rates, effectively restraining or stimulating economic activity.

This sets the direction of availability of liquidity in the market but also the cost of capital that will flow throughout the financial system. You see, it all goes back to risk-premium. When the FED is conducting quantitative tightening (QT), AKA restraining economic activity, they raise the cost of credit (i.e. IORB, RRP, SOFR, Discount window). They’ll raise the hurdle rate by utilizing their arsenal of aforementioned monetary tools to maintain the level of liquidity in the private- and -public sector’s balance sheet. How the financial sector reacts highly depends on their willingness to take on excess risk (risk premium).

For the most part, investors understand that when the FED switches the flip and is conducting QT, the financial sector will be undergoing higher rates and growth suppression. Vice versa when they conduct quantitative easing (QE), the Fed pushes liquidity into the system by acquiring the bank reserves on their own balance sheet. It's a very simplistic accounting overview of how these tools work, but nevertheless significant to understand when monitoring liquidity flows.

Commercial Banking and Money Management

For banks, the dynamics of high rates bring a two-pronged effect. On one hand, they stand to earn more on the loans they issue due to the higher rates. On the other hand, the demand for loans could diminish as businesses and consumers hold back due to the steep borrowing costs. Moreover, the risk profile of potential borrowers might change. In a high-interest environment, those seeking loans might be the ones who are unable to finance their needs through other means, potentially leading to a riskier pool of borrowers. Consequently, banks might tighten their lending standards, further reducing the availability of credit in the market.

Conversely, when rates are low, the cost of borrowing becomes cheaper. This environment can act as a catalyst for economic activity. Businesses might find previously unviable projects now profitable, given the lower financing costs. They might ramp up investments, leading to job creation and increased production. For consumers, low rates might make it easier to finance homes, cars, or education, stimulating demand across various sectors.

Banks, in a low-interest-rate scenario, might see a surge in loan demand. However, the profitability of each loan might be reduced due to the lower rates. Yet, the increased volume could compensate for these thinner margins. Additionally, the general optimism in a low-rate environment could lead to an influx of creditworthy borrowers, allowing banks to maintain or even relax their lending standards.

Everyone’s a Money Magician

Banks also have the power to create money out of thin air. Let’s use Alice as an example, who decides to buy a house and needs a $100,000 loan, she approaches a bank, let's call it Bank A. After assessing her creditworthiness, Bank A agrees to grant her the loan. Contrary to popular belief, Bank A doesn't lend out someone else's deposited money. Instead, it effectively creates this loan "from thin air." In banking terms, this means creating a new deposit in Alice's account while simultaneously recognizing the loan as an asset on its balance sheet.

Accounting Mechanics: From an accounting perspective, every loan transaction has two sides. On Bank A's balance sheet, the loan to Alice becomes an asset because it represents money she owes them. Simultaneously, the deposit they've placed in Alice's account is a liability because it's money the bank owes to her. So, Bank A's assets have increased by $100,000 (the loan) and its liabilities have also increased by $100,000 (the deposit).

Paraphrasing Joseph's Wang (free course on his website - link), “Banks are able to create money, but they are constrained by the size and composition of their balance sheet. It is something they must take into account when proceeding with lending/borrowing. These mechanisms were instilled in response to GFC in order to create balance sheet stability - reforms known as: Basel 3.”

The profile of the Balance sheet is vulnerable to constraints, these include:

Asset Quality - Capital ratio (Risk Weighted Assets)

Size - Supplemental Leverage Ratio (SLR), FDIC leverage Ratio

Liquidity - Liquidity Coverage Ratio (LCR), Net Stable Funding Ratio (NFSR).

The Federal Reserve doesn’t directly finance these individual loan transactions. However, central banks play an indirect role. As Joseph eluded to, If there are reserve requirements, a portion of Alice's deposit may need to be held as reserves. If Alice decides to spend her deposit and it ends up in another bank, Bank B, then Bank A might need to transfer reserves to Bank B. If Bank A doesn't have sufficient reserves, it can borrow them from other banks or the Federal Reserve. In recent times, many central banks, including the Federal Reserve, have shifted away from strict reserve requirements, focusing instead on broader liquidity and capital requirements to ensure bank stability.

Liquidity Management: Beyond the balance sheet, banks need to manage liquidity. If Alice decides to transfer her deposit to another institution or makes a large purchase, Bank A must ensure it has sufficient funds (or reserves) to meet that transfer. This necessity to settle interbank transfers or withdrawals underscores the importance of liquidity management in banking.

A large part of this multifaceted banking industry falls under the control of the top levels of this hierarchy. It sort of forms the foundation of how money is created and distributed. To note, it is a very simplistic schematic of how the system undergoes the open market operations. Hence why I termed the article Part 1 of a multi informational series. They set the mood for how the economy will progress.

NeuroInvest has its own proprietary methods of diagnosing liquidity in the financial system, so if you are interested in that, definitely follow the research page on Twitter (X) . I hope to keep expanding the page and provide more details in the financial world, through quantitative eyes. If you enjoyed the article, found it useful or have any questions please share, hit the like and subscribe button!

References and Relevant Information

https://fiscaldata.treasury.gov/americas-finance-guide/federal-spending/

Regulatory Incentives and Quarter-End Dynamics in the Repo Market

Bank Balance Sheet - Central Banking 101 (Free Video)

The QT Timebomb - Fed Guy - QT led to market weakness

The Federal Reserve’s Market Functioning Purchases - Market Functioning Channel

Central Banking 101 - Joseph Wang

Thanks for sharing this great summary! Do you have any explanation as to why the Treasury continues to issue short-term debt instead longer-term debt given the inverted yield curve? Does this have anything to do with liquidity demand from the financial markets?

Great question. Issuing LT debt depends largely on the markets tolerance to risk AKA duration. Secondly financing LT debt is harder, there are less available liquidity channels (i.e RRP) to fund transactions, which answers your second question - yes demand for monetizing LT debt is more impactful on the broader market. If the market absorbs LT debt poorly, yields rise and discount gets repirced.